Financial Freedom Series

How to Achieve Financial Freedom – Part 4

I hope that you are well on your way to experiencing control over your finances through what we have reviewed over the last few weeks. Firstly by learning how to spend on purpose by looking at your spending habits in Part 1, also by setting up automatic transfers to paying yourself first and saving money as we learned in Part 2 , then by understanding Debt and compound interest in Part 3 so that you aren’t putting money in someone else’s pocket. Now we want to briefly touch on working on eliminating debt to reduce your outstanding credit obligations.

Reducing and Eliminating Debt

Outstanding consumer debt gives you sleepless nights, and creates stress in your daily life. The best night of sleep you will have is when you do not have any consumer debt.

Remember: Good debt is when you have debt for appreciating assets or investments. Bad debt is when you have debt for regular purchases or depreciating assets.

You need to reduce or eliminate the bad debt in order to be able to put more money in your pocket. The first step is understanding debt, and if you went through the exercises last week, you know what interest rates your are being charged on each of your credit cards.

If you have outstanding balances on any of your credit cards or lines or credit, you need to make monthly payments on all of them, but not equally. Determine what is reasonable for monthly payments within your budget and pay the minimum monthly payments on all the cards, but pay an additional amount on the card that charges the highest interest. Once that card is paid off then you use the excess money to pay off the second card, and so forth until all your consumer debt is paid off.

Through this process, you should also start to think about future purchases and ensure that if you can’t pay for it on the spot, then you should wait until you have saved the money in order to purchase it. Like I mentioned last week, use your credit card, but you should have the money in the bank to pay for that particular purchase.

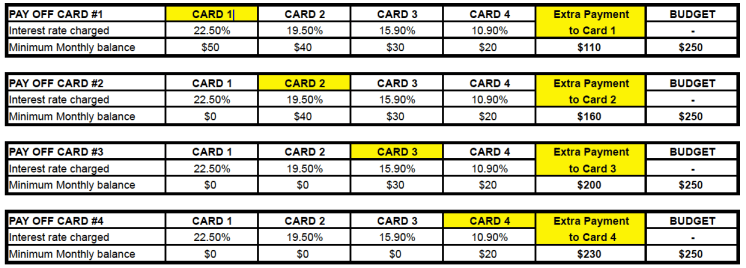

For eliminating debt, you need to budget an amount for eliminating debt. This amount remains the same and always gets used each month until all your debt is paid off. Below outlines an example of paying off your credit cards, in the instance you have 4 credit cards with balances on them.

Example:

- You have 4 credit cards with outstanding balances.

- You have determined from your budget that you can put $250 towards monthly payments on your credit card.

- All four cards have different interest rates: 22.5%, 19.5%, 15.9%, and 10.9% with minimum balances of $50, $40, $30, & $20 respectively.

- The minimum payment balances total $140.00 per month for all four cards, so from your budget you have an additional $110 to put towards paying off your debt.

- The surplus ($110) is to be an extra payment on the credit card with the highest interest rate. So you would put $110 surplus + $50 minimum payment = $160 payment on the card with highest interest rate each month until balance is paid off in full.

- Once that card is paid off in full – keep it that way and pay that balance off monthly moving forward.

- Then apply the amount of the surplus to the minimum amount you were paying on the card with the second highest interest rate. So you would submit $160 (surplus amount once Credit card #1 is paid off) to Card #2 with the $40 minimum payment. Making a total payment of $200 to credit card.

- Keep rolling over that budget amount to the next outstanding credit card with the third highest interest rate, and so forth, until all debt is paid off.

- See example charted below

Eliminating consumer debt is one of the most freeing things you will experience. Once you have eliminated that debt, your budget amount for debt payments then goes right into your savings, which you can then invest in order to grow the money and use for your future retirement, or save for things you really want to do – travel? experiences?

Work on getting that debt reduced and eventually eliminated by putting these tips into action for yourself, and we’ll see you soon to discuss Part 5 in your journey to Financial Freedom.